market news & Natural resource equities

US Markets registered modest gains on Monday. The Dow Jones Industrial Average closed 34,006.88 +43.04 (+0.13%) while the Nasdaq Composite closed 13271.32 +59.51 (+0.45%). European and Asian stocks slid along with US futures after yields on 10-year Treasuries rose to their highest since 2007. A gauge of Chinese property developers slumped after Evergrande missed payment on an onshore bond. The dollar rose, while Brent fell.

Jamie Dimon warned the world may not be prepared for a worst-case scenario of the Fed raising rates to 7% along with stagflation. "Going from zero to 2% was almost no increase. Going from zero to 5% caught some people off guard, but no one would have taken 5% out of the realm of possibility," he told the Times of India in Mumbai. "I am not sure if the world is prepared for 7%."

GOP and Democratic negotiators in the Senate are nearing a deal on a short-term spending measure that would keep the government open after Oct. 1, a person familiar said. The legislation would extend funding for 4-6 weeks, a shorter time frame than the Democrats wanted. A US shutdown would be negative for its credit rating, Moody's warned — the only major credit grader to assign the country a top rating.

The Fed will need to raise rates one more time this year and keep policy tighter for longer if the US economy is stronger than expected, Neel Kashkari said. The Minneapolis Fed president said he was one of the 12 policymakers who forecast another hike this year in projections released after the central bank's meeting last week.

Hedge funds ramped up wagers against stocks to drive down their net leverage — a gauge of risk appetite that measures long versus short positions — by 4.2 percentage points to 50.1%, according to Goldman's prime brokerage. That's the biggest week-on-week decline in portfolio leverage since 2020. JPMorgan's Marko Kolanovic said retailers, automakers and airlines will take the biggest hit as their pricing power wanes on falling inflation.

The EU's new, tougher approach to China is being shaped by French concerns that Beijing's trade practices have started to pose a critical threat to core industries. People familiar said that Paris has taken a key role in driving the policy shift, fearing that Europe's auto sector is vulnerable to Chinese imports in the same way that the solar industry was a decade ago.

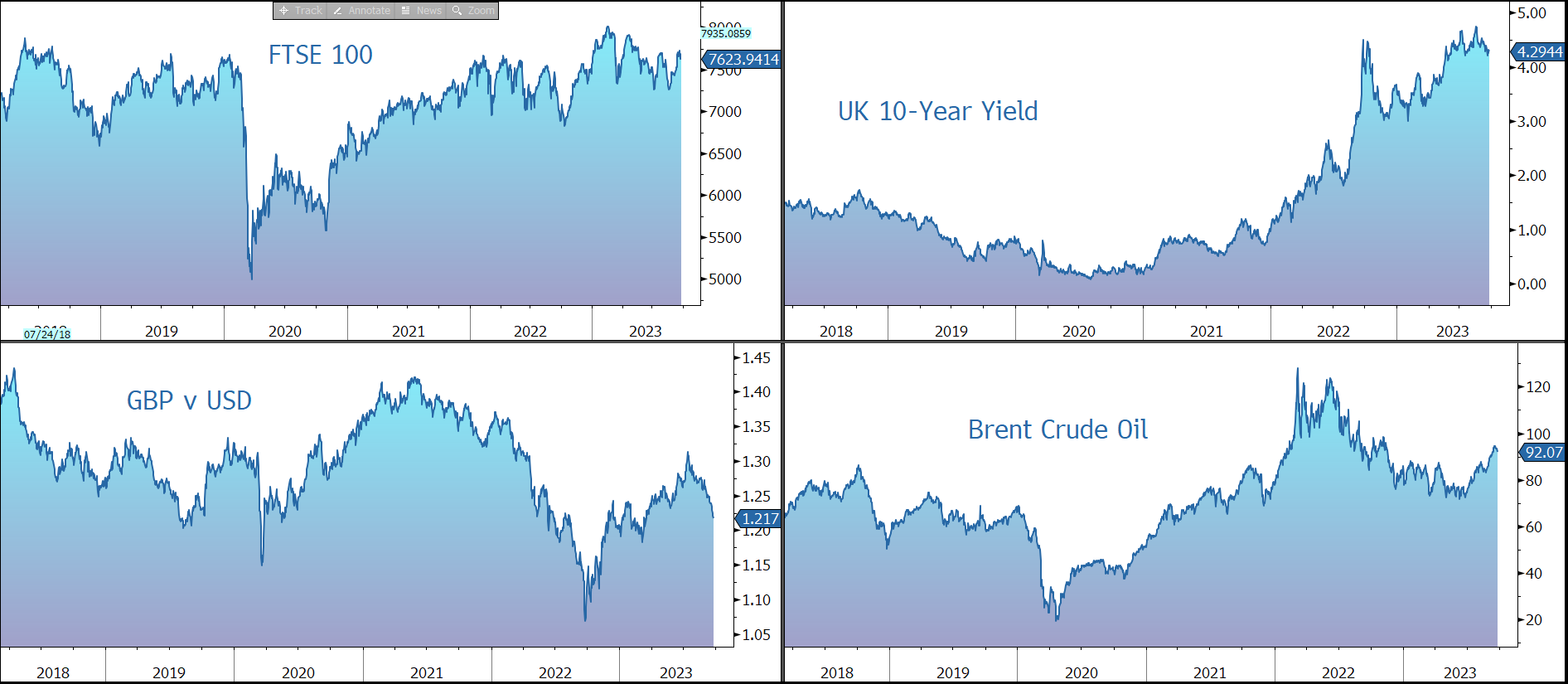

Source: Bloomberg

Natural Resource Equities

After a period of good performance following The Pandemic, where inflation and inflation expectations began to rise and investors were looking for companies that would benefit from a shift to an inflationary regime, natural resource stocks been lacklustre and energy stocks have only recently started to perform after a weak first half of 2023. The reason for this was a shift in investor perceptions about the risk of a global recession. Both energy and materials are highly sensitive to the global economy, hence the rotation out of these areas. Perhaps the best example of this price action was the Global Financial Crisis (GFC) in 2008-09 when these sectors were hit particularly hard. However, while there are some similarities to post-GFC era that rightly give investors cause for concern, in many ways the two periods are very different.

Firstly, in the run up to the Global Financial Crisis (GFC) in 2008, the “commodities super-cycle” driven by insatiable demand from China was in full swing. This meant that the commodity capital cycle was similarly expanding as companies responded to higher prices with investment to bring new supply on stream. The capex cycle in commodities is very long with new investment often taking many years or even decades to come on stream. When the bust arrived and demand took a hit, it did so at a time when supply was ramping up and given the price inelasticity in many of these markets, the impact on prices was significant. The lag effect of supply coming on stream meant that even as the economy recovered, commodities entered a protracted bear market, that would continue for another decade.

Today the situation could not be more different. This time, as the economy turns down, the brutal bear market has seen capex in these sectors cut to the bone. This time there will be no aggressive supply response augmenting the weak demand in terms of price pressure. For the companies, capital discipline has been the order of the day and this, combined with the time lag for any spending to bear fruit, means there is little chance of that changing in the years ahead. In the GFC, the capex cycle and the economic cycle were reinforcing. Today they are working in the opposite direction.

Secondly, resource stocks and commodities are inexpensive when compared to financial assets. Large oil and materials extraction companies trade on low single-digit price/earnings multiples, indicating that the market has little confidence that the current commodity prices can be maintained. Prices of the underlying commodities don’t need to appreciate for these companies to make excellent returns, they only need to not collapse, which given the underlying demand-supply situation is highly unlikely.

In a world where financial assets are expensive, at the very least resource stocks provide a significant margin for error. Furthermore, the returns the companies are making are not being squandered – capital discipline is strong with surplus cash flows being used to pay generous dividends and buy back shares.

Thirdly, despite the bounce since The Pandemic lows, energy and materials make up only around 7% of the S&P 500. This compares to around 18% at the previous peak just before the GFC. That the price of these key inputs makes up such a small percentage of the economic value belies their importance. They are the building blocks upon which all economic activity is based. In 2022, we had our first small peek at what life might look like when their supply is restricted. Closet and explicit indexation woefully mis-represents this reality within most portfolios.

Investors whose reflexive instincts, instilled in them by recent history, to flee these sectors based solely upon a highly justified fear around the future economic growth prospects, are not factoring in the full picture and are ignoring one of the few areas of the market with the potential to provide genuine diversification.

Source: Bloomberg